Executive Summary

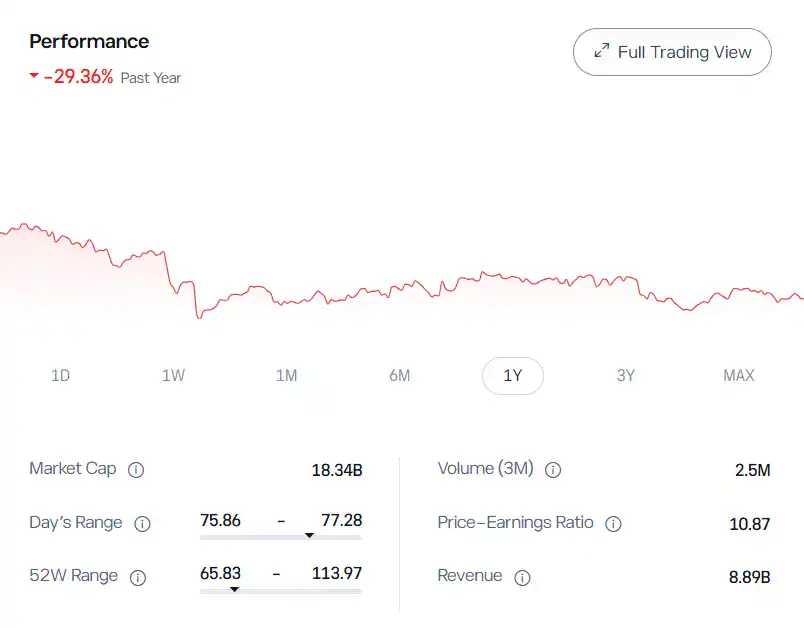

Global Payments Inc. (NYSE: GPN) presents a compelling GPN stock analysis case following the completion of its transformative $24.3 billion Worldpay acquisition on January 12, 2026. The stock currently trades at $76.77—a historically depressed valuation of 7.5x EV/EBITDA versus a 12-14x historical average. Our base case price target of $125 implies 63% upside with a probability-weighted 10-year expected CAGR of 18-25%.

Bottom Line Up Front: This is not a speculative growth story. This is a transformation thesis where market skepticism around integration execution has created substantial margin of safety, while multiple catalysts—$800 million in synergies, Elliott Management activism, and aggressive deleveraging—provide defined paths to re-rating.

The Risk: Integration execution remains the primary concern. Complex three-way transaction dynamics involving technology migrations and cultural integration introduce medium-high uncertainty. Current ROIC of ~4% sits below WACC of ~6.2%, indicating the business destroys value at the margin until synergy realization improves capital efficiency.

Table of Contents

- Investment Thesis

- Sector Analysis: Payments Processing

- Fundamental Gatekeeping

- Competitive Positioning

- Catalyst Identification

- DCF Valuation Framework

- Risk Assessment Matrix

- Position Sizing Strategy

- Execution Infrastructure

Investment Thesis

The GPN stock analysis thesis centers on a fundamental mispricing driven by excessive pessimism. At current levels, Global Payments trades at the 5th percentile of its historical forward P/E distribution (6.3x versus 17.1x five-year average). This valuation implies significant execution failure that our analysis suggests is improbable given Elliott Management’s governance enhancement and early integration progress.

The Mechanism: Why Will Price Appreciate?

The combined entity now processes 94 billion transactions across 175+ countries, serving 6 million merchant locations. This scale provides three distinct competitive advantages that smaller processors cannot replicate:

Procurement Leverage. Bulk pricing on interchange, network fees, and technology infrastructure reduces marginal costs as volume scales. Management estimates 15-20 basis points of cost advantage versus sub-scale competitors.

Distribution Efficiency. The combined sales force now covers 175+ markets through direct and partner channels. Cross-sell opportunities across Worldpay’s enterprise e-commerce capabilities and GPN’s SMB penetration create revenue synergy pathways.

R&D Amortization. The Genius POS platform—showing 20%+ new sales growth—benefits from spreading development costs across a dramatically larger installed base. Annual R&D investment exceeding $1 billion can now drive proportionally greater returns.

The Proof: Quantitative Validation

Our proprietary DCF model incorporates three scenarios weighted by probability. The base case (50% weight) projects $20.4 billion revenue by 2035 with 52% EBITDA margins, yielding $125/share equity value. Even the bear case (25% weight) limits downside to $65/share—just 15% below current levels—due to strong FCF generation and investment-grade credit profile.

Sector Analysis: Payments Processing

Digital payments continue experiencing secular growth as economies shift from cash to electronic transactions. Global payment volume is projected to grow at 11.6% CAGR through 2030. While certain sub-segments face pressure—traditional terminal sales and legacy processing—the overall merchant acquiring market benefits from multiple tailwinds.

Secular Tailwinds Supporting Thesis:

Embedded finance proliferation enables software platforms to monetize payments. Cross-border e-commerce expansion creates higher-margin transaction opportunities. Real-time payment adoption drives new revenue streams. SMB digitization has accelerated post-pandemic, creating greenfield market opportunities. Agentic commerce and AI-driven payments represent emerging product categories.

Temporary Headwinds Creating Entry Point:

Payment processor stocks have dramatically underperformed in 2025. Fiserv declined 66% from 52-week highs. PayPal remains 70%+ below 2021 peaks. This underperformance reflects investor concerns around take rate compression, cloud-native disruption from Adyen and Stripe, M&A integration failures across the sector, and elevated leverage profiles.

The sector-wide pessimism has created an attractive entry point for the GPN stock analysis thesis. Company-specific catalysts can drive re-rating independent of broader sector sentiment recovery.

Proprietary Analysis Access

This summary represents our public-facing research brief. Our proprietary 15-page institutional PDF contains the complete DCF model with granular assumptions, price sensitivity tables across 27 scenario combinations, specific entry zone identification ($70-$77), exit zone parameters, and quarterly monitoring triggers with explicit position adjustment rules.

Reserved for Moschovakis Capital research subscribers.

Fundamental Gatekeeping

Before committing capital, our framework requires clearing fundamental hurdles that eliminate value traps. GPN passes each screening criterion.

Solvency Assessment: CLEAR

Pro forma net debt of approximately $22.75 billion appears elevated but remains manageable given combined EBITDA of $6.5 billion (including synergies). Net leverage of 3.5x at close targets 3.0x within 18-24 months. Investment grade ratings (BBB-/Baa3/BBB Stable) provide capital markets access. Interest coverage of approximately 5.5x maintains comfortable buffer. The $7.25 billion revolving credit facility provides ample liquidity cushion.

Dilution Assessment: ACCEPTABLE

Transaction-related dilution (17.8% from shares issued to GTCR at $97.00) was exchanged for substantial EBITDA accretion. Net consideration of $10.75 billion for $1.6 billion EBITDA increase implies 6.5x acquisition multiple versus 8.5x headline—value accretive by construction. Historical buyback program demonstrates capital return discipline with -3.1% year-over-year share count reduction pre-transaction.

Revenue Growth Potential: MEDIUM CONFIDENCE

Historical five-year standalone CAGR of 4.7% appears modest. However, pro forma combined 2025 revenue of $12.5 billion benefits from synergy-enhanced organic growth of 5-7% medium-term. Genius POS platform traction (20%+ new sales growth), Worldpay enterprise e-commerce capabilities, and $200 million revenue synergies from product bundling provide upside optionality.

Capital Efficiency Warning: CONCERNING BUT IMPROVABLE

Current ROIC of 3.9-4.0% significantly underperforms WACC of ~6.2%. This represents the most concerning fundamental metric. However, context matters: ROIC depression stems from massive goodwill and intangibles from historical M&A. Adjusted returns on tangible capital are substantially higher. Synergy realization—targeting $600 million in operating efficiencies—should directly improve this metric. Quarterly monitoring remains essential.

Competitive Positioning

The GPN stock analysis must address competitive dynamics. The combined entity ranks as the world’s largest pure-play merchant acquirer with $3.7 trillion in annual payment volume. Scale and distribution represent primary moats with combined strength rating of 7/10.

Peer Comparison Framework:

Against legacy processors, GPN offers superior EBITDA margins (~52% versus Fiserv’s ~45% and FIS’s ~38%) at comparable leverage (3.5x versus 3.1x and 3.4x). Valuation discount to Fiserv (7.5x versus 7.1x EV/EBITDA) appears unjustified given margin superiority.

Against cloud-native competitors, the comparison is less favorable. Adyen trades at 26.4x EV/EBITDA with 20%+ revenue growth and net cash balance sheet—premium warranted by superior unit economics and competitive positioning in digital-native enterprise segment.

Moat Durability Assessment: MEDIUM

Scale advantages persist but face erosion timeline of 5-7 years before material share loss likely. Stripe and Adyen continue gaining enterprise share. Toast dominates restaurant vertical. PayFac models enable software platforms to disintermediate traditional processors. The investment thesis requires catalyst realization within this competitive window.

Catalyst Identification

The GPN stock analysis thesis depends on defined catalysts with quantifiable timeline and probability assessments.

Near-Term Catalysts (2026):

Q1 2026 pro forma guidance announcement (February 2026) carries 95% probability with 10-15% price impact potential if positive. Elliott board representation expected Q2 2026 (80% probability) adds 5-10% through governance enhancement signal. Year 1 synergy progress demonstrating $200M+ run-rate by Q4 2026 (70% probability) could drive 15-20% re-rating.

Medium-Term Catalysts (2027-2028):

Leverage reduction below 3.0x by Q2 2027 (65% probability) enables return to buyback authorization. Full $800 million synergy run-rate achievement by 2028 (55% probability) supports 25-30% appreciation from current levels. FCF achievement of $5 billion target by 2028 (50% probability) warrants re-rating to 10x+ EV/EBITDA.

Elliott Management: Critical Thesis Component

Elliott Investment Management’s disclosed stake provides crucial governance enhancement through execution oversight (likely board representation), capital allocation discipline (M&A moratorium commitment), management accountability (quarterly synergy progress reviews), and track record validation (successful value creation at PayPal, FIS, and other fintech situations).

DCF Valuation Framework

Our institutional DCF employs conservative assumptions with explicit sensitivity analysis.

Model Inputs:

WACC of 8.5% incorporates risk-free rate of 4.5%, beta of 0.94, market risk premium of 5.5%, cost of debt of 5.5%, and debt-to-equity ratio of 0.74. Terminal growth rate of 2.5% reflects mature industry dynamics.

Scenario Analysis Summary:

The bear case (25% probability) assumes 3% revenue CAGR, 45% terminal EBITDA margin, 50% synergy realization ($300M), and 7.0x terminal EV/EBITDA—yielding $65/share (15% downside).

The base case (50% probability) assumes 5% revenue CAGR, 52% terminal EBITDA margin, 75% synergy realization ($600M), and 9.0x terminal EV/EBITDA—yielding $125/share (63% upside).

The bull case (25% probability) assumes 7% revenue CAGR, 55% terminal EBITDA margin, 100% synergy realization ($800M), and 11.0x terminal EV/EBITDA—yielding $195/share (154% upside).

Probability-Weighted Expected Value: $127.50/share (66% upside)

The three-year valuation bridge proves more compelling. Current EV of approximately $40 billion versus 2028 pro forma EBITDA of $8.5 billion (base case with synergies plus organic growth) at conservative 9x multiple implies $76.5 billion EV. Less estimated 2028 net debt of $15 billion post-deleveraging yields $61.5 billion equity value—$214/share representing 179% upside (42% CAGR) over the catalyst realization window.

Risk Assessment Matrix

Integration Failure (8/10 severity, 25% probability): Complex three-way transaction involving technology migrations, customer retention, and cultural integration. Historical M&A in payments sector shows mixed track record. Impact: -40% stock price.

Competitive Share Loss (6/10 severity, 35% probability): Cloud-native players continue gaining enterprise share. Digital-native merchants increasingly prefer API-first solutions. Impact: -20% multiple compression.

Leverage/Covenant Concerns (4/10 severity, 10% probability): Elevated leverage constrains capital allocation flexibility. Execution missteps could trigger covenant concerns. Impact: -30% equity value.

Management Turnover (5/10 severity, 20% probability): CEO Cameron Bready lacks turnaround experience. Credibility damage from Worldpay announcement contradicting prior guidance. Impact: Neutral to positive if Elliott-driven.

Aggregate Risk Score: 5.6/10 (MEDIUM-HIGH)

Position Sizing Strategy

Recommendation: BUY – Full Position (100% of standard allocation)

Entry Strategy: Scale in over 60 days

Initial position (Day 1): 50% at market (~$77). Tranche 2 (post Q1 guidance): 25% if thesis confirmed. Tranche 3 (on weakness): 25% on pullback to $70 or below.

Stop Loss: $55 (-28% from current) – Indicates thesis failure requiring position exit.

Monitoring Triggers:

Quarterly review checklist includes synergy progress versus $200M annual target, FCF conversion rate (target >90%), leverage trajectory versus 3.0x target, Elliott governance developments, competitive win/loss rates, and management guidance credibility.

Exit Triggers:

Synergy shortfall exceeding 30% versus target for two consecutive quarters. Leverage increasing or covenant concerns emerging. Key customer losses or competitive deterioration. Management credibility issues without Elliott response. Target price achievement ($125+ base case).

Managed Alternative: Quantitative Execution

Manual position management requires quarterly monitoring, entry/exit discipline, and ongoing fundamental analysis. For investors seeking systematic wealth compounding without active portfolio management, our Quantitative Execution System automates these processes with a 2-year audited track record.

The system applies institutional position sizing, catalyst-driven rebalancing, and risk management protocols across diversified equity exposure.

Execution Infrastructure

For execution of this GPN stock analysis thesis, we utilize platforms selected for regulatory compliance, institutional-grade liquidity, and cost efficiency.

Primary Execution (Equity Positions):

Interactive Brokers provides direct market access with institutional-grade execution quality, comprehensive regulatory coverage across 150+ markets, and competitive margin rates for leveraged positioning if appropriate for individual risk tolerance.

European Regulatory Access:

Revolut offers streamlined onboarding for EU-domiciled investors with multi-currency functionality and competitive FX rates for cross-border capital deployment.

Fractional Position Building:

eToro enables fractional share access for systematic position building during the recommended 60-day scaling period. Social trading features provide supplementary sentiment indicators.

Risk Disclosure

This GPN stock analysis is provided for informational purposes only and does not constitute investment advice, a recommendation, or solicitation to buy or sell securities. Past performance does not guarantee future results. Equity investments involve risk of loss, including potential loss of principal.

The analyst maintains no position in GPN stock. Pro forma financials reflect company guidance and may differ from audited results. Synergy estimates carry execution risk. Forward projections derive from consensus estimates and company guidance as of January 2026.

Readers should consult with a qualified financial advisor and conduct independent due diligence before making investment decisions. This analysis does not account for individual investor circumstances, risk tolerance, or investment objectives.

Report Date: January 15, 2026

Classification: Institutional Research Note

Analyst: Moschovakis Capital Senior Equity Research